The fall of the Roman Empire created a vacuum where safety and efficiency had once been taken for granted. Without the Roman military authority, medieval European commerce was left in a disrupted state. The crusades, unrecognized territorial boundaries and disputed sea rights made dependable trade difficult and reduced local merchants’ access to product. Out of this chaos, emerging monarchies, seeking to provide for the basic needs of their populations, were compelled to create a partnership framework for trade.

The fall of the Roman Empire created a vacuum where safety and efficiency had once been taken for granted. Without the Roman military authority, medieval European commerce was left in a disrupted state. The crusades, unrecognized territorial boundaries and disputed sea rights made dependable trade difficult and reduced local merchants’ access to product. Out of this chaos, emerging monarchies, seeking to provide for the basic needs of their populations, were compelled to create a partnership framework for trade.

The ensuing commerce network grew out of a desire to open the aperture to ever larger markets where buyers and sellers could transact. Monarchs granted market licenses to merchants, who arranged with carriers and transport ships to deliver goods, provided by distant farmers, ranchers or purveyors of metals, spices, silk, or other foreign wares. Demand funnels consolidated, creating efficiencies within supply chains, consequently facilitating even more utility throughout the growing networks – globalization is deflationary.

The Marketplace Evolution Is Not New

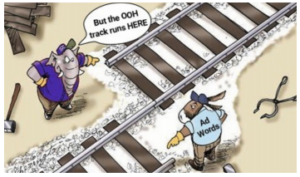

Today we find the same dynamic in the digital advertising ecosystem. A few large corporations manage proprietary advertising networks. While close, no single group yet controls the modern global marketplace as the Romans or Greeks once did in the ancient world. For everyone else, the advertising ecosystem follows medieval practices. We can view the current OOH media marketplace as a relatively provincial service. It has been provided without the benefit of the scaled digital ad networks, which were established out of necessity, and are governed by wellestablished protocols for trading.

How To Play

To underwrite any change in direction, one requires a plan, conviction, and in lucky cases, a model to follow. The plan below, outlines the tactical steps required to move OOH into the enormous contemporary digital ad marketplace. It takes its cues from the mobile advertising ecosystem. Their rules have already been written and the membership requirements are clear.

To underwrite any change in direction, one requires a plan, conviction, and in lucky cases, a model to follow. The plan below, outlines the tactical steps required to move OOH into the enormous contemporary digital ad marketplace. It takes its cues from the mobile advertising ecosystem. Their rules have already been written and the membership requirements are clear.

NOTE: These principles apply to all location-based OOH assets. Small-format digital signs, large-format printed billboards and even adhesive posters provide access to audiences. They may each differ in terms of utility, but all can be evaluated based upon their ability to deliver against a brand’s objective. Printed signs remain very effective products. They deliver a constant set of impressions 24/7 for an average of 4 weeks – like turning a digital sign to a single piece of creative. As such, printed frames can be individually evaluated and bought from within the digital marketing ecosystem.

Why?

The mobile advertising market has grown from $3 billion in 2011 to a projected $224 billion by year end 2021. In 2022 it is expected to represent almost $250 billion globally exceeding all other individual forms of media.

Mobile developed efficient tools of trade. Publishers only began building their connected ecosystem when mobile devices broke into the mainstream – 10 years ago. Despite mobile’s unique attributes, their architects drafted early development off of the desktop ad-market, which itself was only established around the turn of the millennium. Mobile has its idiosyncrasies both positive and negative. Its small formats are off-set by location-based advantages relative to desktop media while commanding a significant share of attention perday per-person. We can learn and follow best practices here.

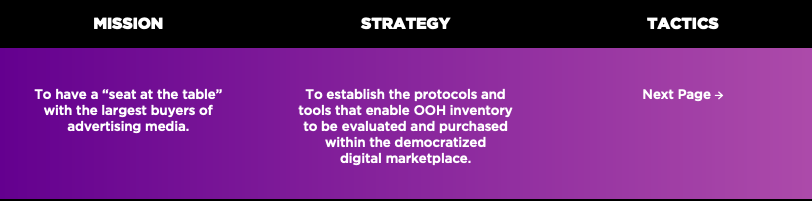

In order for the OOH industry to gain access to the ever increasing $100s of billions being spent in the digital advertising world, we must get in the game. OOH publishers and specialist buyers should not be satisfied with a simple return to CPI growth-rates and business-as-usual, post-covid – regardless of how comfortable that might seem sitting in the pandemic today. If we wish to achieve exponential exit velocity, it is essential that we commit to the “house” rules. Our unmistakable mission is to be included in the strategic-level marketing discussions and the massive ad budgets that are set from there.

As we decide how to build our future, we must be careful not to write our own rules. Siloed thinking does not work. OOH is not so unique that is requires a completely different thesis – and buyers will not belabor unnatural hurdles to find it.

OOH Is Powerful

OOH is not burdened by viewability concerns, brand safety issues, personal intrusion, ad fraud/click bots, measurement games, ad blocking, multi-channel monopolies, etc.

OOH media can enhance customer experiences with amazing creative. OOH enables convenient adjacent on-the-go information earning the attention of consumers (traffic, directions, weather, vaccine availability, etc.). It is inherently location-based. Our canvases are massive printed and digital opportunities to deliver messages at a point in a decisionjourney, where customers are most receptive to inspiration. Unlike digital media, our inventory is finite, and it provides location-exclusivity to targeted audiences.

OOH provides opportunities throughout the marketing funnel. Our medium can now expand well beyond brand awareness campaigns – a fact which needs to be sold. Technology advancements, more thoughtful distributions using data, smarter creative techniques, and partnerships with mobile media, will drive considerable incremental utility.

We have an opportunity to enable perfect transparency, simple buying mechanisms, and the comparative-value crossplatform measurement call-to-arms that P&G’s Marc Pritchard P&G seeks².

All of this accrues to a value that is underappreciated by marketers (having been undersold since folks wrote on cave walls). To date we have not had the tools to make compelling arguments regarding the value offered by OOH, relative to other forms of media.

Mobile media has been bought and sold based on a publishers’ ability to guarantee a set number of impressions, to a targeted audience group, that delivers a specific message, aligned to achieve a defined goal. For OOH to participate in this larger marketplace, we must do just that.

-

Measurement

What is not measured, is not valued. The global media standard, the single currency for all media regardless of the medium, is impression counting. Every marketer needs to know how many potential customers are being reached through a particular opportunity (TV, CTV, Search, OOH, etc.) and how to segment them. It all begins and ends with impressions. These impressions need to be counted with standards that can be relied upon by marketers to be accurate and provided in such a way as to facilitate cross-media value comparisons.

A / Facilitating Channel

1. Provided in commonly accepted formats to assist buyers as they evaluate the efficacy and value of each media format being considered.

2. Sufficiently granular and “real-time” as to enable reconciliations between media planning and a campaign’s actual delivery. Real-time enough to also provide for dynamic campaign management (moving creative between locations to efficiently capture impressions), inter-campaign progress reporting, financial-period reporting, etc.

3. Provided in an ingestible format to be used by multiple parties across the planning, purchasing, publishing and the proof stages of advertising.

4. Accredited by a neutral body as to the counting methodologies, data sourcing, extrapolations, etc. such as the MRC. 5. Delivered with transparency to engender trust amongst all parties 6. Offer utility without violating privacy standards for data gathering 7. Completed against a curated set of frames that has been audited for the accuracy of their view-sheds. -

Value Matrix

Not all impressions are equal. Impressions in one medium are potentially more valuable than another. Impressions generated within one audience segment may be more/less valuable to a specific advertiser or campaign. An impression captured within connected TV delivers sight, sound, and motion. Mobile impressions are clickable and precision targetable. On the other hand, OOH can be unavoidable 14 by 48-foot behemoths. As we mentioned above, all types of media also have their drawbacks. To establish a framework for relative value, marketers assign a CPM (cost per 1000 impressions) to each media based on the specific needs of that campaign. Our account executive teams need to help establish the value of OOH in those dynamic matrices by highlighting the nature of unique impressions captured by our assets. We need to communicate the utility of OOH to media buyers – relative to other media alternatives – based on the specifics of the individual campaign objectives being considered – as we participate in those planning discussions. Once complete, the matrix analysis will highlight the gap in value between OOH and other alternatives, giving us further opportunity to discuss adjustments to CPMs accordingly.

-

Audiences

Once we can count impressions, they need to be segmented for demographic and behavioral targeting. Adding to the criteria for impressions counting above, measured impressions need to be delivered in such a form that they can be included into any of four buckets. — Basic demographic segmentations (e.g., 18-35 females, …) — Ingested into 3rd party audience products (Claritas, Acxiom Personics, etc.) — Custom demographic and behavioral allocations based on client needs (18-35 soccer moms that like gardening, …) — Matched with 1st-party data targeting provided by marketers (required to identify specific OOH locations where that unique custom audience can be reached.)

-

Establish Legal Framework

The ability to trade media in the contemporary digital ecosystem requires that legal standards be established and maintained to facilitate the ease of trading. Publishers must provide for a clients’ ability to trade based upon location and time as currently done (e.g., a particular board for a 4-week period), and/or based on the delivery of a number of impressions. Impression buys can be limited to location(s) over a specific period or garnered from any number of locations to which the targeted audience migrates throughout the day/week/period – “dynamic campaigns.”

1. Impression buys may be guaranteed or non-guaranteed; putting an additional burden on publishers to deliver according to, and requiring, the measured counts above.

2. For each transaction, buyers and sellers must accept and agree upon an impressions counting source and audience segmentation provider for delivery. Legal liability must be established as to diligence for the data providers and any real or perceived dependencies. Accredited counting methods facilitate easier agreements (MRC).

3. Advertiser contracts need to be “clickable” in order to facilitate a mobile-like fast-paced trading environment. Trading partners pre-agree to most terms based on the type of buy being considered, with only basic campaign parameters being filled into each new contract.

4. Publishers and buyers need to establish a framework to resolve under/over-delivery scenarios. Make goods, rebates, bonuses, etc.

5. Contracts with real estate landlords, where assets are represented by publishers, must also consider impressions-based buying as revenue-share components will need to consider different revenue recognition components. If a digital campaign is dynamic, and ads are being moved from board to board to “chase” audiences, value from one board to another must be allocated according to the number of impressions captured at each location during its time in market. 6. Transparency in pricing throughout the value chain – disclosed from brand to publisher – including fees, discounts, and participations in any agency relationship programs -

Establish A Financial Framework

Just like the legal framework, modernizing the financial systems of OOH publishers is critical. Location and time have been the basic sales “product” within OOH since the business’ inception. In order to add an impressions component, several changes to financial systems need to be undertaken.

1. Revenue recognition methodologies which reflect the legal buy/sell agreement must be created

2. Potential make-goods, bonuses or other solves for under/over-delivery of contracted impressions need to be represented in balance sheet reporting

3. Modified contract administration and reporting to advertising clients/agencies, landlords, auditors, and publishers’ financial stakeholders must be instituted

4. Proof of performance (POP) criteria needs to be established, standards observed and reconciliations to contractual commitments monitored. Most campaigns are being run across multiple publishers – consolidating POP reporting with others will be important – requiring systems integration, consistent counting etc.

5. Post campaign reports sent to clients/agencies need to include actual performance relative to contracted terms.

All of this depends upon basic enabling technologies. -

Technical Capabilities and Integrations

Each publisher will be required to more closely integrate their systems with the digital marketplace. Overall technical roadmaps can be easily separated into two buckets; (a) sales channel integrations for planning and accepting orders, and (b) the back-office engines required to produce the services provided.

A / Facilitating Channels

The 4 main execution channels are relatively simple and open the aperture between publishers and advertising buyers. Transactions can be facilitated in any manner best agreed upon between the parties without restrictions on sales – making OOH easier to buy. Each of the 4 channels provides buyers with access to inventory availability, pricing, associated impressions data, location attributes, etc. through slightly different portals.

1. Account Executive Tools – Publisher account executives and marketing teams need to have live access, via a company research & planning user interface (UI), to the inventory available – in such a manner as to give the teams the ability to tailor packages in real-time for buyers that fit with brands’ specific campaign needs.

2. Direct Digital Connections – Some large buyers and agencies will be best suited to “pull” relevant information directly into their own sophisticated systems via an API connection. Those agencies can then evaluate specific publisher inventory against available inventory from other OOH publishers and/or other media options – implementing the OpenDirect standards now under consideration. This is the fastest and likely the least expensive channel, once established.

3. Programmatic – “Programmatic” does not mean the robots are coming to take over the world (or jobs from sales folks). Programmatic simply refers to a separate channel where third parties facilitate the connection between a buyer and a seller of media. Publishers make inventory available to a Supply Side Platform who in turn makes that inventory available, in real time, to connected buyers called Demand Side Platforms into which brands and agencies are integrated. The efficiency in this model is derived from organizing the myriad of market participants, and the technology investment made by the platforms, to facilitate trading environments. Fees paid to both DSPs and SSPs along this chain, can significantly reduce the aggregate value of media purchased given a set dollar budget; but, it may be just compensation for efficiency and suspected incremental spend from new buyers.

— Resellers – can be included in this category. Resellers increase a publisher’s reach to buyers with whom the publisher may not be familiar, and/ or provide more efficient access, at a lower cost, to many smaller buyers.

4. Client Self-Serve – similar to the direct connections mentioned above but targeted to small agencies and local buyers who prefer to shop / transact on their own. Each of the data sets above can be provided via a userfriendly web-based interface or via a mobile app. Each facilitate greater access to inventory and additional demand on assets; but they do not generate the demand itself.B / Modernized Back Office

We need a new engine room. The technology stacks within OOH have not received the investment or attention that would be required to change our trajectory as a business. Printed and digital frames can all be digitally enabled to be bought and sold along-side other forms of advertising.

1. Centralized inventory availability

2. Dynamic query capabilities

3. Automated pricing tools

4. Product catalogs

5. Sales workflow = Research & Planning > shopping cart > proposal > contracting > financial reporting systems

6. Creative workflow = creation > traffic > approvals > posting > POP to follow the previously contracted terms

7. Digital hardware that is easily inter-operable with overall systems and that produce high confidence and

8. Proof-of-performance delivery and revenue recognition integrations, data capture and analytics

9. Implement any other IT standards including modernizing Data Governance, off-prem cloud storage, etc.…

10. Contemporary digital displays must be capable of two-way communication for POP from the screen, remote health monitoring, and “smart” enough for complex dynamic campaigns -

Objective Based Selling

Last, but the most important – regardless of the technical integrations, the sophisticated data being provided, or the legal and financial frameworks established, as an industry, we will benefit most from providing clients with a tailored solution that helps them achieve their business objectives. As a medium we have been largely “bought” using ‘spray and pray’ strategies rather than “sold” as a precision-based tool used to achieve a goal set upon by a brand. OOH was, and is still largely perceived, as a brand-building medium at the top of the decision funnel. That myopic thinking ignores the significant value that can be provided by OOH to achieve clients’ targeted objectives and it devalues our medium by a factor.

1. Measured impressions give us a way to compare how we reach potential customers, and to engage with ad buyers in a manner consistent with all other media sales strategies.

2. With impression counts, and sophisticated research and planning tool sets using that data, we can elevate sales conversations with buyers and their agencies – pushing discussions up into the strategy and planning stage far in advance of the commencement of campaigns

3. OOH can be complimentary and/or provide supplementary media to other buys being considered in CTV, mobile, search, desktop, radio, etc. – but it needs to be explained and “sold” in connection with other media and a defined objective.

4. OOH sales teams must begin with knowing the brand-customer intimately. We need to have a close understanding of their objectives (increased foot traffic, increased basket size, brand repositioning, targeted new customer acquisition, product launch, etc.) We must also appreciate timing, total spend, alternative market signals, brand sensitivities, and anything else relevant to launch a public message. With this information, the desired targeting information agreed with the brand, and the tools mentioned above, OOH sales teams can help create strategies to craft campaigns in real time along-side the client with confidence in the efficacy of OOH. This is consultative selling.

5. We must create constant learning environments and hire a generation of sellers that appreciate the underlying value of OOH and its ability to advance marketers’ objectives – using the digital tools and the protocols of the larger contemporary advertising marketplace.

6. We believe that OOH is undervalued. Today we may be able to compliment other media at lower price points, in order to bring campaign average CPMs down and showcase OOH’s value. However, these tactics above, taken together, enable us to have comparative media value discussions and INCREASE the CPMs currently provided by OOH sellers.

7. Some OOH publishers are selling mobile ad-inventory as a complimentary product. The same tactics used to sell mobile campaigns should be used in selling OOH – (impressions-based sales, SARs, value-based, audiences, KPIs, …) These same tools can be applied to OOH in order to sell ever increasing volumes, at higher prices, to more buyers.

8. Channel participation is tertiary – the objective is first, and the campaign is second. Each of the 4 channels mentioned above are just execution paths (yes, even programmatic). SALES is, and will always be, required to fill the pipeline. The selection of an execution channel should be based on availability, cost, and speed.

9. All of this added-value accrues to our ability to command higher CPMs for OOH as an additional source of growth and grants us a platform on which we can do good for our communities. We should be uncomfortable. Breaking new ground is not easy…yet we should be confident in our product. These tactics and having faith in a path already set forth by mobile-advertising, give us the necessary strength of conviction.

For many years it has been said that OOH needs to be easier to buy. OOH has also lacked the measurement data and research tools essential to engage in thoughtful discussions about the value and the efficacy of our medium relative to others. I suspect that is about to change³. The combination of these advancements with a proactive objective-oriented sales force, will lead to an exponential opportunity for OOH. Digital enablement is not easy in any sector; but it has an almost unlimited return on investment. Medieval déjà-vu all over again.

Published: July 14, 2021